Cash is always king but never more so than during the pandemic and recovery.

Cash is always king but never more so than during the pandemic and recovery.

Many small businesses are hoarding cash and staying on the sidelines until they feel confident enough to invest in their own growth.

This is a key takeaway from the March 2021 SME Growth Index, with results showing that over the past 12 months substantially fewer small businesses than usual experienced cash flow issues.

This round, 72.5% of small businesses had cash flow problems, compared to the 90% who usually report these issues.

This is perhaps an indication that government COVID-related stimulus measures in 2020 had the desired effect.

However, it still equates to almost three in four small businesses experiencing cash flow issues, despite the low interest rate environment and the extensive SME loan support options available.

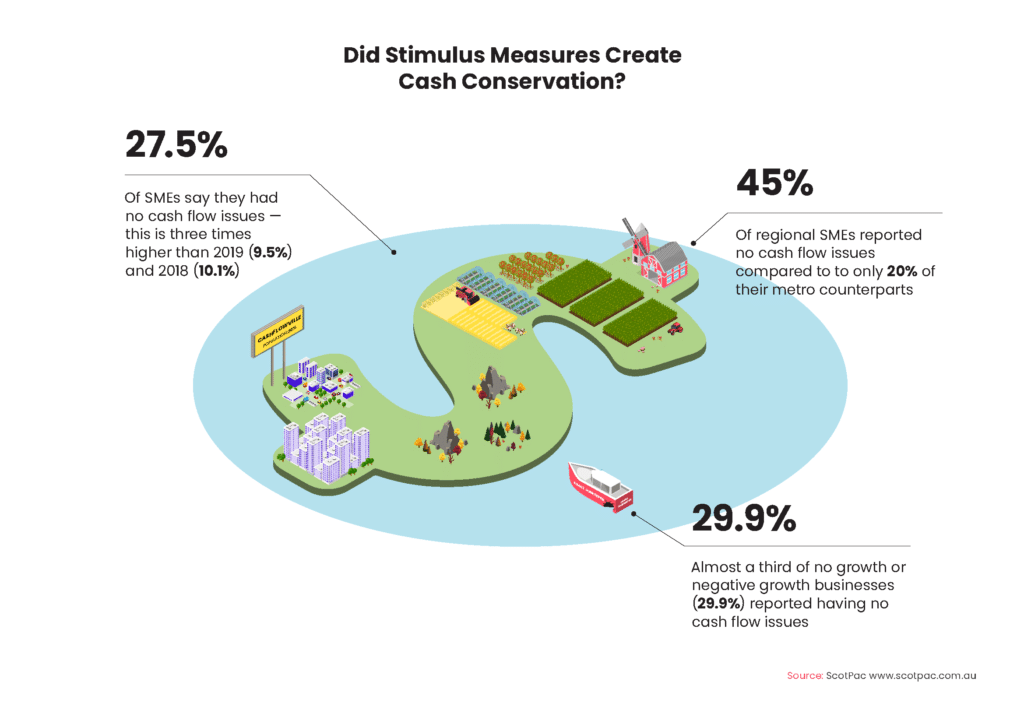

This round a full 27.5% of small businesses had no cash flow woes – this compares to the March 2018 result when 10.1% were free of cash flow issues, while in September 2019 it was 9.5% who reported no cash flow concerns.

This prompts the question – did the pandemic stimulus packages actually improve cash flow for many small businesses?

SMEs definitely appear to have been conserving cash during 2020. For some businesses this was facilitated by government support measures, but for others it looks to have been more about stripping out costs and banking whatever cash they could. This trend is quite similar to the retail savings growth that occurred over the same period.

Given the aim for many businesses in 2020 was simply survival, this cash conservation on face value might not seem like an issue – however, there are longer term implications.

If businesses continue to conserve cash within their enterprises, and if they are not actively looking to invest to help their business grow, they run the risk of becoming less relevant in their market.

The finding that a third of SME respondents are trying to grow revenue via new and existing customers doesn’t gel with the fact that so many are not yet looking to invest in their own businesses to facilitate that growth.

If businesses do have cash reserves off the back of stimulus measures and being more conservative to get through the pandemic, it could be prudent to use those cash reserves to engage an expert adviser to guide them on the right strategies and funding for growth and recovery.

Allowing these cash holdings to be strategically unlocked would bode well for forward investment, including possible job hiring and revenue growth.

Who is reporting no cash flow issues?

Of the 1253 SMEs in the research, 345 of them reported having no cash flow issues. Among them:

- 45% of regional SMEs reported no cash flow issues compared to only 20% of their metro counterparts, which concurs with Commonwealth Bank of Australia analysis about the health of regional Australia.

- A large proportion of the SMEs reporting no cash flow issues are those identifying as negative growth businesses. While the cohort is small, this data point lends weight to the hypothesis that it is the “propped up” SMEs who are on top of cash flow, assisted by cash grants, loan payment deferrals, wage subsidies and asset write-offs.

- Very small businesses appear to be hoarding cash. While the data from this round of the Index generally shows smaller sized SMEs as worse off than their larger sized counterparts, that is not the case for this data point – of the SMEs reporting no cash flow issues, the majority are small (SMEs with one to 20 full-time employees).

What causes cash flow woes

Over the years the Index has consistently highlighted cash flow constraints as one of the top barriers to a healthy business, especially for growth SMEs.

Government red tape and compliance issues remain the most pressing cash flow issue for the whole SME cohort over the past 12 months.

Red tape and compliance (44.3%) was nominated by almost twice as many respondents as the two other top cash flow concerns, difficulty meeting tax payments on time (23.9%) and failed credit applications (22.9%).

A further 16.5% of businesses struggled with cash flow when their credit lines were reduced, and 14.6% were unable to take on new work due to cash flow restrictions. These factors may have had the effect of prolonging the COVID downturn for many small businesses.

The strain of greater outcomings and fewer incomings was evident, with reduced supplier payment terms causing cash flow issues for 20.8% of respondents and late customer invoice payments creating problems for 20% of businesses.

With JobKeeper no longer in place it is likely that the low number of firms currently reporting cash flow concerns due to bad debts (3.9%), losing key debtors (3.8%) or losing key suppliers (1.6%) may push higher during 2021.

Top cash flow strategies

In the wake of the pandemic small businesses have outlined the strategies they will use to manage their working capital in 2021.

Common strategies range from cash flow forecasting, to making arrangements with the ATO and putting in place cash flow friendly funding such as invoice finance.

From the whole SME cohort, 27.8% plan to focus on cash flow forecasts; this strategy is much more prevalent amongst larger SMEs (it will be utilised by 48.6% of large SMEs, but only 9.1% of small SMEs).

Outside of the response options, respondents wrote in the next two most popular strategies – focusing on existing customers to grow revenue (27.5%) and expanding with new customers (21.8%).

Almost one in five SMEs (17.2%) say they will make special arrangements with the ATO regarding tax payments.

Another common way to manage working capital is to use invoice finance to smooth out cash flow peaks and troughs (a plan nominated by 15.6% of SMEs).

More than one in 10 (11.7%) say they will take out or increase their overdraft, while a similar number (11.6%) will seek out online funding providers.

Of concern is the response by more than one in 10 business owners (11.6%) that they will manage working capital by relying on personal finances such as credit cards.

This confirms that many small businesses have ingrained credit accessibility issues, despite the deluge of COVID-related stimulus measures.